Have Investors Benefited From Momentum Strategies?

by P.J. DiNuzzo September 4, 2018

Have Investors Benefited From Momentum Strategies?

MOMENTUM CHARACTERISTICS ARE SHORT-LIVED

Momentum premiums have been studied extensively since they were first documented by Jegadeesh and Titman in 1993. Simulated momentum strategies typically have high average returns, but they also have high turnover. The latter is expected, given that momentum characteristics tend to change quickly. As Exhibit 1 illustrates, the momentum premium decays rapidly. For example, 10-12 months after classification as high momentum, the excess return of upward momentum stocks was no longer positive on average. Whether such a high turnover premium can survive implementation costs remains an empirical question.

DO MOMENTUM FUNDS CAPTURE MOMENTUM?

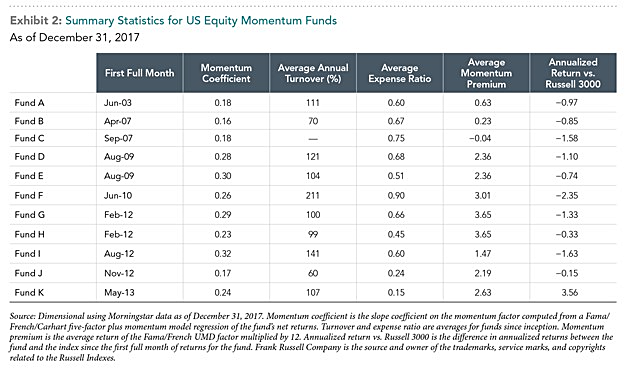

Examining the performance of live mutual funds helps us assess the real-world profitability of momentum strategies. We identified funds in Morningstar's US equity category with "momentum" in their name and at least 36 months of returns. We excluded multi-factor funds to ensure the funds chosen have a pronounced focus on momentum. Summary statistics for the final sample of 11 funds are presented in Exhibit 2.

As the momentum coefficient column indicates, these strategies have had relatively high exposure to the momentum premium. Average turnover was generally high, consistent with the academic evidence around momentum premiums. The second-to-last column reports the average momentum premium for each fund during the period analyzed. Most of these strategies have experienced a strong momentum premium as measured by the average return of the Fama/French UMD factor, and yet, as the final column indicates, the vast majority were unable to convert favorable premium performance into higher-than-market returns, after fees and expenses.

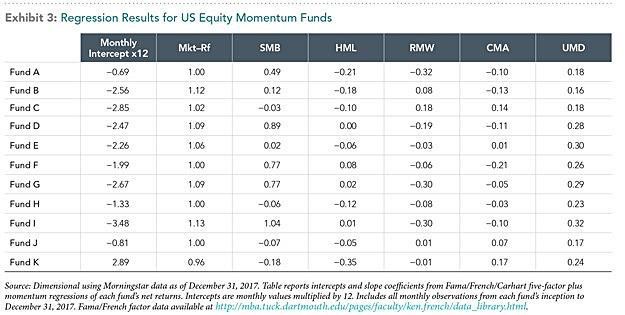

Comparing the performance of momentum funds to the Russell 3000 Index allows investors to assess whether the funds have outperformed the broad US market. Another way to benchmark momentum funds is to regress their returns on a factor model that controls for known drivers of expected returns, including momentum. Exhibit 3 reports intercepts and slope coefficients from regressions using a Fama/French/Carhart five-factor plus momentum model. Again, we see that most of the momentum funds have underperformed, with only one having positive regression intercepts.

A SENSIBLE WAY TO USE MOMENTUM INFORMATION

Most mutual funds focusing on momentum have not been able to capture the momentum premium after costs, even when the premium was positive. Does this mean that investors should ignore momentum? Not at all. Rather than pursuing it directly, however, we believe they should consider momentum at the point of trade. Using momentum signals to inform buy and sell decisions can enhance returns when the momentum premium is positive, without incurring high and costly turnover.

DATA APPENDIX

Upward Momentum Stock Returns

Data: CRSP and Bloomberg. Large caps in the US includes stocks listed on NYSE, AMEX, and NASDAQ with market equity greater than the median market equity of NYSE-listed stocks. Large caps in non US developed market includes stocks within the top 90% of market capitalization of each country. Large caps in emerging markets includes stocks within the top 90% of market capitalization of each country. Within each country, stocks are sorted based on total return over the previous 12 months, excluding the most recent month (the "lookback period"). Stocks with total returns over the lookback period above the 70th percentile are considered up momentum. Rebalanced monthly. Filters were applied to data retroactively and with the benefit of hindsight. Groups of stocks are hypothetical, are not representative of indices, actual investments or actual strategies managed by Dimensional, and do not reflect costs and fees associated with an actual investment. Actual investment returns may be lower. Past performance, including hypothetical performance, is no guarantee of future results. S&P data © 2018 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. MSCI data © MSCI 2018, all rights reserved.

Sincerely,

P.J. DiNuzzo, CPA, PFS, AIF®, MBA, MSTx

President, Founder, and Chief Investment Officer